Dante's Inflation Part II

Thank you for joining us for this edition of the NovaBlock newsletter. Here, we explore the intersection of technology, finance, politics, and of course, the crypto asset space.

Just like the frog being boiled alive as the water temperature gradually reaches boiling point, we are in inflation purgatory as it erodes our purchasing power and distorts spending and investment habits. In Dante’s Inflation Part I, I discussed inflation, its pernicious effects on society, and how market and government forces are using it to prop up asset prices.

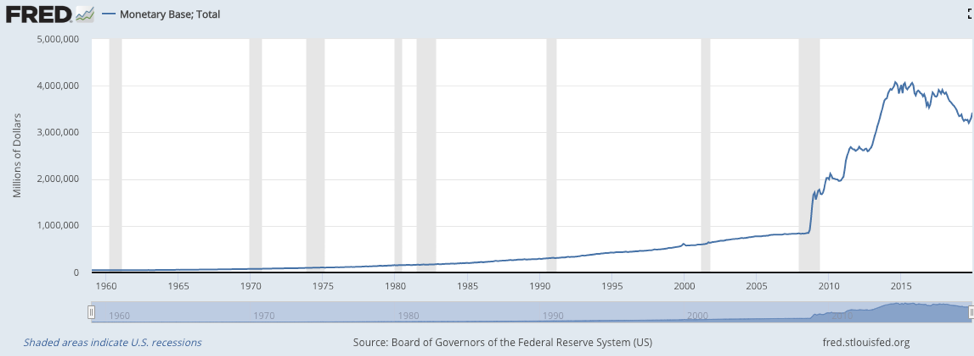

If you’ve been following the newsletter, you’ve seen the chart below several times already. In the wake of the Great Recession of 2008, the Federal Reserve has undertaken an unprecedented expansion of the US monetary base. This has been accomplished through several rounds of quantitative easing in which the Fed purchased toxic assets to the tune of trillions of dollars, financed with newly minted USD.

As the monetary base rapidly expanded, we would expect consumer inflation to pick up as the economy is flushed with newly minted cash. Surprisingly, this has yet to be the case and reported inflation rates have been low.

The government has endorsed the Personal Consumption Expenditures Price Index (PCE) and the Consumer Price Index (CPI) as the basis for measuring inflation and conducting monetary and fiscal policy. Over time, the basket of goods comprising CPI grew to a bloated list of 80,000+ items, muting dramatic price changes in common goods and services. Furthermore, CPI excludes items such as taxes, energy, and food; which are not only necessities, but often the majority of daily expenditures.

The PCE inflation rate hovered around 1.6% in 2019. The question remains: if the Fed has been firing up the money printer, why have official inflation estimates been tepid and unable to reach the Fed’s 2% annual target?

Source: https://fred.stlouisfed.org/series/BPCCRO1Q156NBEA

A paper published in June 2019 by economists from Harvard and Princeton concluded prices accounting for nearly half of the PCE price index don’t respond to changes in economic activity. In 2017, economists at the Federal Reserve Bank of San Francisco found these “acyclical” goods and services comprised an astounding 58% of the index.

Due to the pitfalls of baseline inflation metrics, economists have attempted to create indices that more accurately reflect the rise of every day goods and services. One such metric is the Chapwood Index. The Index attempts to measure the true cost of living by reporting the actual price increase of 500 items on which most Americans spend their after-tax money. Some of these items include Starbucks coffee, Advil, insurance, gasoline, sales and income taxes, fast food restaurants, pizza, cellphone services, laundry detergent, light bulbs, pet food, underwear and People magazine.

Remarkably, the Chapwood Index reported average annual inflation of 11.4%, 11.7%, and 10.9% in New York City, Los Angeles, and Chicago respectively for the last 5 years. This clearly tells a different story from the reported sub-2% rates.

But let’s consider for a moment the government is correct and annual inflation really is sitting below 2%. An important concept affecting inflation is the velocity of money, which indicates how newly printed money moves through the system.

Although the monetary base has ballooned to over $3 trillion, we may be seeing low inflation because monetary policy acts with a lag. An increase in the money supply will inevitably lead to higher inflation; however, the velocity of money determines the lag. When banks are lending, businesses are borrowing, and consumers are spending, money exchanges hands quickly. Under these conditions, monetary velocity is high and inflation rises.

Conversely, when banks refuse to lend, businesses are hunkered down, and consumers are saving or paying down debt, money velocity is low and does not lead to greater exchange of goods and services. Hence, delayed inflation.

So, if this capital is not stimulating economic growth and spending, where is it going?

Much of the new capital injected into the economy has directly flowed towards wealthy asset owners by propping up asset prices. As the majority of this new capital is locked in financial markets, the velocity of money is low, which suppresses real inflation. When the Fed artificially pins interest rates near 0%, savvy corporate managers are incentivized to arbitrage low rates by borrowing and using the funds to buy back their corporate stock.

Source: https://www.visualcapitalist.com/stock-buybacks-explained/

Stock buybacks is a common practice that has its pros and cons. The practice is an alternative to dividend payments and serves as another way for companies to deliver returns to shareholders. As expected, companies that engaged in stock buybacks outperformed their peers. However, the practice exacerbates wealth inequality and enriches shareholders, whereas the company instead could use those funds to grow their business and make longer term investments.

Source: https://www.visualcapitalist.com/stock-buybacks-explained/

Furthermore, low interest rates drive down returns in bonds, certificates of deposit, and money market accounts, forcing institutional and retail investors to flock to riskier investments and asset classes to find greater returns. High dividend equities become inflated for the same reason. These companies are pressured to continue paying high dividends instead of reinvesting profits into the business, otherwise the stock price will crash. The search for yield is everlasting and increasingly harder to find.

This charade of new capital flowing into financial markets is leading to unprecedented paper gains amongst asset owners, which is unsustainable and cracks are starting to show. The Fed has displayed their commitment to keep the party going at all costs, exacerbating the divide. We never know when the bubble will pop, or even what will serve as the pin. However, Bitcoin is emerging as the ultimate hedge to these market distortions. There is no ambiguity around Bitcoin’s monetary policy. Anyone can run a node and verify Bitcoin’s supply and issuance rate. In recent months and years, Bitcoin has demonstrated it is transitioning from a risky asset to a safe haven, store-of-value asset and it will continue to prove itself in the face of political and economic uncertainty.

Quick Bits

SEC commissioner Hester Pierce proposed a three-year “safe harbor period” for startups conducting token sales. This would give crypto businesses and startups time to build out their network and reach sufficient decentralization before the SEC determines whether they need to comply with the agency’s securities laws. Although this is only a proposal, crypto projects have responded positively as it would introduce a grace period allowing developers to build projects without needing to worry about securities regulations. This would be a huge development for the industry, as the SEC has yet to provide guidance, instead pursuing punitive action against some of the largest players such as EOS and Telegram.

DeFi has reached its largest milestone yet breaking $1 billion in total value locked in DeFi protocols and platforms. Total value locked has increased rapidly, up 50% year-to-date. The industry has converged on total value locked as a crude metric to measure the growth of the DeFi space. Since these platforms are over-collateralized and require digital assets as collateral, total value locked demonstrates the inherent value of digital assets to power decentralized financial contracts.

Lightning Labs raised a $10 million Series A round to be the Visa of Bitcoin. It is using the raise to gear up the launch of its first paid service for merchants seeking to accept Bitcoin payments. Lightning Labs released a beta version of the scaling solution LND in 2018 and previously raised $2.5 million in a seed round from investors Twitter CEO Jack Dorsey, Square executive Jacqueline Reses, Litecoin creator Charlie Lee, and former PayPal COO David Sacks. The Lightning Network is a foundational scaling technology that will enable Bitcoin users to send and receive payments instantly with near zero fees. Scaling initiatives and second layer solutions like Lightning are adding additional utility to Bitcoin and enabling the Bitcoin economy.