The Safe Haven of Bitcoin

Thanks for joining us for this edition of the NovaBlock newsletter. Here, we explore the intersection of technology, finance, politics, and of course, the crypto asset space.

Although today’s current financial dogma declares the major equity indices should provide average annual yields of 8-10% over the long run, public equities are rife with volatility and commonly experience 30-40% drawdowns in contractionary scenarios. Several prolific investors have come out of the woodwork exclaiming passive investing is its own bubble, suggesting the days of buying and holding an equity index and expecting consistent double digit returns may be a thing of the past. Today, there are many reasons to be wary of the stock market: increased political and trade tensions between China and US, corporate stock buybacks propping up the markets, weak ISM manufacturing and services data, each interest rate cut and round of QE lessening the Fed’s ability to stave off the impending recession, and a host of other reasons we will explore in future issues.

Safe haven assets are specific investment assets investors perceive to have relative stability, and even upside potential, during times of economic and political distress. It is a type of investment that can be relied on to retain and even increase in value, while other assets are falling. In order to maintain a sufficiently diversified portfolio, maintain wealth, and curb risk (volatility), savvy investors seek assets that are non-correlated or negatively correlated to the general market. Historically, safe haven assets included gold, treasury bills, defensive stocks, and cash.

So, if safe haven assets are so desirable, why don’t investors allocate more capital to them instead of the traditional stocks and bonds portfolio mix? The problem is identifying them at the right time and acting on it. Safe haven assets can change quite rapidly decade to decade, in fact, government bonds used to be considered one of the safest investments. In 1987, the S&P500 lost 33% of its value peak to trough, whereas the 1-year treasury bill had a yield of 6-7% the same year. However, bond yields are trending towards zero and may even reach negative territory, especially if the US follows the path of Europe and Asia. Thirty percent of all investment-grade securities now offer negative yields, meaning investors purchasing the debt and holding to maturity are guaranteed to realize a loss.

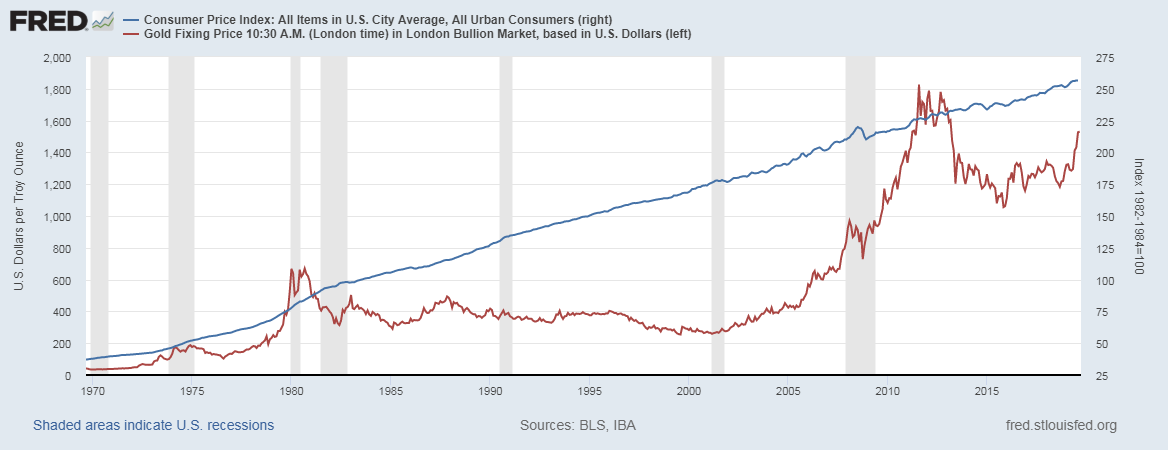

Gold is perceived to be the ultimate safe haven asset, outlasting entire civilizations over millennia. As a physical commodity, it cannot be printed like money, and its value is not impacted by monetary policy decisions made by any government regime. It is often believed that gold is a hedge against monetary inflation, as it has perceived relative scarcity and a low annual inflation rate of ~2%. The problem is when you look at the actual data, gold does not seem to be following the narrative “gold as inflation protection” as of late.

Since the 1970s and the first iterations of gold funds, the US consumer price index (CPI) has been on a linear trajectory, while it took gold over 25 years to get back to breakeven (in nominal terms) if one bought gold as a safe haven during the 1980 recession. Since the 1930s and the Great Depression, gold had a ~3% annual return after inflation. Hardly an impressive investment.

(Credit to Andrew Gillick of BraveNewCoin for suggesting this point)

In our view, Bitcoin is emerging as the next safe haven asset with a value proposition that strengthens as economic and political instability increases. Bitcoin is not a safe haven asset quite yet, as it is volatile and has numerous growing pains and attack vectors that must be addressed. However, it has the characteristics to improve upon gold’s deficiencies, and every day it continues to produce blocks of transactions, it becomes increasingly antifragile. Over the course of the next few years and decades, as Bitcoin increases in scale and adoption, it will become more stable and reliable as a global store of value.

As of today, Bitcoin has no ETF, and little central bank and institutional exposure. This reduces cross-ownership and interconnections with other parts of the financial system, explaining its non-correlation with other asset classes. Bitcoin’s relative insulation from the wider financial system should make it a safe haven from shocks emanating from that system. While Bitcoin has its own native risks, they are largely independent from the global financial system.

Bitcoin is a digital commodity that is fundamentally scarce with a supply cap of 21 million and issuance rate that halves every four years. It is highly portable, divisible, and censorship resistant. As a digital bearer asset, it is difficult to seize by tyrants or corrupt government officials. A refugee fleeing her country can transfer all of her wealth just by memorizing a list of 12 words. Furthermore, Bitcoin represents a global pool of liquidity that citizens of corrupt nation-states can tap into and protect against adverse capital controls or hyperinflationary regimes.

Even though these sound like extreme scenarios, it would be awfully foolish and ignorant of history to assume similar events cannot transpire in developed countries, especially considering the current state of the union. As the 2020s fast approaches and we reach unprecedented levels of economic and political uncertainty, which safe haven will you choose to store your wealth?

Quick Hits

The NBA shuts down Spencer Dinwiddie’s bid to tokenize his professional contract. The professional Brooklyn Nets player sought to turn his $34 million contract into a tokenized bond, allowing accredited investors to participate in the player’s performance and earn interest on the investment vehicle. However, the NBA responded by blocking the motion, and it remains unclear if it will ever move forward. We applaud Dinwiddie’s attempt, and we expect similar innovative financial vehicles to be proposed and eventually succeed in the near future.

Germany’s federal finance minister supports Digital Euro, but is against private currency projects like Facebook’s Libra. Minister Olaf Scholz stated an e-euro would be beneficial for Europe’s financial system, particularly in the wake of economic globalization. Scholz argued the power of currency issuance should reside in the hands of the state and denounced private currency initiatives. In our view, private currency issuances are inevitable and will fundamentally disrupt the status quo political and economic structures. Thus, it is unsurprising heads of state are alarmed and are starting to voice their criticisms.

Class action accuses Tether and Bitfinex of market manipulation. A New York based legal firm filed a lawsuit against Tether and Bitfinex accusing them of cryptocurrency market manipulation. Tether is a one-to-base USD backed stablecoin tied to the value of the of the dollar. The suit alleges Tether was not fully backed one-to-one by the dollar, and Bitfinex fraudulently printed Tether to profit off market volatility. Correlation doesn’t mean causation. Supporters of this claim point to large Tether issuances often coinciding with large market swings. However, it would logically fit that market volatility leads crypto traders demanding more Tether. Regardless of the outcome, getting to the bottom of this will be healthy for the maturation of the space.