Dante's Inflation

Thanks for joining us in the inaugural issue of the NovaBlock newsletter. Here, we explore the intersection of technology, finance, politics, and of course, the crypto asset space. In this issue, we provide a few musings on the concept of inflation and we interview Scott Purcell, CEO of Prime Trust, one of the leading crypto asset custodians.

What’s the big deal about inflation?

Every macroeconomics 101 course teaches that moderate inflation is an indicator of a healthy economy, whereas, deflation is something that should be avoided at all costs. Inflation is the decline in purchasing power of a particular fiat currency. It is quantitatively measured using the price of a basket of selected goods and services in an economy over a certain period of time. The basket of goods includes food, housing, medical care, and other goods and services. The most commonly used inflation indices are the Consumer Price Index (CPI) and the Wholesale Price Index (WPI).

The Federal Reserve maintains a dual mandate for monetary policy – maximum employment and price stability. To meet the price stability objective, Fed policymakers target an annual inflation rate of 2%. Inflation cannot be viewed in isolation to determine economic health, and it carries significant tradeoffs that have tangible financial impact on individuals and institutions.

Inflation erodes a currency’s value over time. In the near term, this can stimulate the economy as it encourages consumers to purchase more today and discourages saving into the future. A consumer contemplating purchasing a car is incentivized to do so today if the value of her dollars will decrease tomorrow, increasing the cost of the car tomorrow. According to Keynesian economic theory, moderate inflation is the byproduct of a healthy economy and represents productivity growth. That is why, in order to stimulate economic growth, the Fed may engage in quantitative easing and lower interest rates, leading to additional inflation (more on that below).

As an opposing viewpoint, Austrian economists view inflation more negatively. They define inflation not as the rise in prices, but rather as the rise in the quantity of money and bank credit. This is an important distinction, as the Austrian’s definition explains the causal relationship: an increase in the supply of money and credit leads to higher prices. They argue inflation discourages saving and encourages high time preference consumption. High time preference consumption prioritizes consuming goods and services today and foregoing future consumption. Low time preference sacrifices consumption today in favor of investment and greater consumption in the future.

This explains why companies that are able to increase capital expenditure often endure as they allocate capital to increase future productivity. Allocating resources to R&D and capital acquisition leads to technological advancement and greater competitive advantage. According to this study analyzing R&D expenditure across 15 countries between 1990-2013, every 1% increase in R&D spending grew GDP by 0.61%.

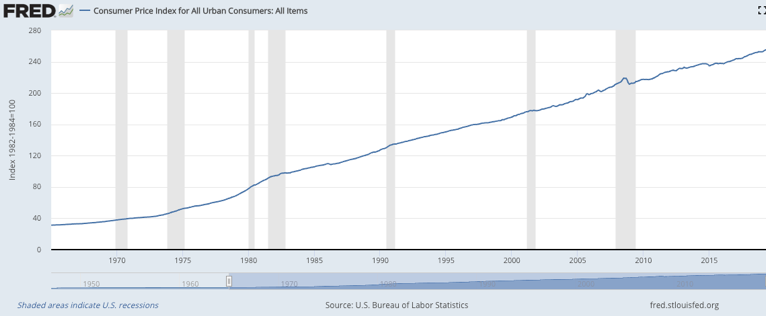

Figure 1: CPI (all items)

Figure 2: Monetary Base (sum of currency outside Fed and Treasury)

The average annual inflation rate in the last 100 years is 3.22%. At this rate, prices double every 20 years. In the past century, the US experienced several decades of high inflation: 103% in the 1970s, 70% in the 1940s, and 62% in the 1980s.

https://inflationdata.com/Inflation/Inflation_Rate/Long_Term_Inflation.asp

Interestingly, the high inflation period of the 70s immediately followed the Nixon shock in 1971, which included wage and price freezes, surcharges on imports, and the unilateral cancellation of the direct convertibility of the US dollar to gold. This effectively cancelled the Gold Standard by replacing the Bretton Woods monetary system with the current fiat monetary system. From that point onwards, the dollar was no longer readily exchangeable for gold, and it would solely have value as “legal tender” decreed by the federal government.

In real terms, inflation makes debt cheaper, whereas deflation makes debt more expensive. In order for a country to pay off its national debt, it must raise taxes and/or allocate funds from the national budget, issue new bonds to pay off existing ones, or print money. The first option represents fiscal conservatism and shifts funds away from other uses such as funding entitlement programs. The second option involves refinancing existing loans and borrowing more money to be paid off at a future date, kicking the can down the road. The third option debases the national currency as new supply floods the market, leading to additional inflation. If recent history is any guide, the US will opt to use a combination of the second and third options to deal with its $22 trillion (and climbing) national debt. As ludicrous as it may sound, the US Treasury is exploring issuing debt with maturity up to 100 years to help meet its obligations, a practice that hasn’t been working so well for investors in Argentina.

Inflation has a tangential effect of increasing the value of investment assets, benefitting wealthy asset owners. As the Fed engages in quantitative easing and pumps money into the economy, much of the new capital goes towards bidding up asset prices through corporate stock buybacks. Low interest rates drive down returns in bonds, CDs, and money market accounts, forcing investors to flock to relatively riskier investments to find greater returns. High dividend equities become inflated for the same reason. These companies are pressured to keep paying high dividends instead of reinvesting profits into the business, otherwise the stock price will crash. Similarly, reducing interest rates make corporate debt cheaper and provide a lifeline for zombie companies to continue to survive. On the surface, this may not sound so bad except that nearly half of US citizens do not own any equities. In fact, 40% of Americans are unable to cover an emergency $400 expense.

As the Sino-American trade wars continue to escalate, we are seeing competition not just on the manufacturing and production front, but also in regards to monetary policy. Both the US and China have incentives to debase their local currency as depreciation stimulates exports and foreign direct investment, effectively weaponizing Central Bank actions. These actions cannot continue indefinitely, and asset bubbles will continue to blow up and burst, with or without the help of central authorities. Individuals often cannot choose which currency they must interact with on a daily basis, however, we are seeing the emergence of optionality in the form of new scarce digital assets with a fixed supply, which may serve as the new de facto safe haven asset class.

Spotlight Interview - Scott Purcell (CEO, Prime Trust)

NB: For all of our readers, please introduce yourself and describe what Prime Trust is aiming to accomplish.

SP: I’m the Founder, CEO and Chief Trust Officer of Prime Trust. Prior to founding Prime Trust, my career has been as a serial entrepreneur in the securities, banking, trust and internet-technology industries. I founded Prime Trust on the premise that, starting with the JOBS Act, and more recently with the advent of blockchain technology, the world is poised for massive disruption of the status quo in our capital markets. My company provides the technology-driven, financial application building blocks for innovators and entrepreneurs to create some amazing businesses that take advantage of this once-in-a-lifetime widow of opportunity.

NB: What are the main products and services you offer today? What do you expect to offer in the future?

SP: The FinTech building blocks we provide as a financial institution include funds processing (wire, ACH, check, credit/debit cards, SWIFT, Bitcoin and Ethereum), compliance-as-a-service (KYC, AML, & Bad Actor Checks), custody of private securities and crypto, escrow for securities offerings, escrow for lending, escrow for transactions, issuance investor transaction technology, issuance offering accounting, processing of investor interest and other repayments, and account-types which include omnibus, asset custody, IRA, college savings and asset protection trusts.

NB: What is PrimeX? What does it enable for your customers?

SP: The Prime Exchange Network (“PrimeX”) is a toolset which enables exchanges, ATS’, OTC trading desks and other customers to frictionlessly move fiat and other assets between accounts. This enables secure, instant settlement of transactions 24/7 between their own segregated accounts, as well as between counterparties.

NB: Where do you see the most traction and adoption in the crypto space?

SP: Currently the main focus is on people, both retail and institutional, who are speculating on investments in Bitcoin and other asset-less, non-security tokens. Security tokens, and asset-backed tokens are still in their infancy, but that will accelerate over time.

NB: What is keeping institutions from jumping in? Are there specific pieces of infrastructure that need to be built that currently don’t exist?

SP: There are numerous reasons why institutions are largely delaying participation in the space. Some is lack of custody services that meet their “big company” requirements, as the current custodians are all young trust companies with nominal capital. This will change as well regarded, highly capitalized firms like Fidelity and Northern Trust enter the space to offer custody services. Another reason is that many investment mangers don’t regard Bitcoin or other current crypto to be investable asset types. This too will change as hard assets like real estate, and as equity and debt securities of businesses become tokenized.

NB: How would you describe your customer base? What types of institutions and companies do you cater to?

SP: Prime Trust has a focus of B2B2C. Thus our customers are crypto exchanges and OTC desks, issuance platforms, crowdfunding platforms, broker-dealers, real estate syndicators and other such businesses. From a regulatory perspective their retail and institutional customers are in fact Prime Trust customer, the practical application is that we require our API-integrated, business customers to maintain the front-facing websites and relationships. We are very good at B2B and have no intention of marketing our services directly to consumers or institutions.

NB: In your mind, what is the main killer use case of blockchain and crypto? Do you see this changing in the future?

SP: Oh wow, that’s a huge question. In my opinion, Blockchain changes everything when it comes to data…that includes not just financial services but also healthcare, environment, housing, legal, and so many other industries. For the industry that is my sandbox, I’m most excited about how blockchain can be used to tokenize assets, especially securities, and how it can enable cross-custodian settlement of transactions without the need for a DTC-like infrastructure, which will bring about a brave new world of ATS’ and liquidity for private securities (and real estate).

NB: How do you view the regulatory landscape shaping up? As a leading custodian and trust company, is Prime Trust taking a leading role in engaging with regulators and shaping best practices around compliance and custody?

SP: Regulators are still wrestling with this, as any ATS will tell you. They tend to look at things through a public-securities lens when it comes to trading and markets, and this new generation of liquidity platforms for private securities has them stuck. I’ve personally provided comments to the SEC on custody and trading, and we’ve worked with FINRA on numerous ATS applications. This is all very embryonic and unclear – lots of risk for early movers, and also lots of opportunity.

NB: You recently hired the Deputy Banking Commissioner of Wyoming, Amanda Ortega. What is the significance of hiring her and what does she bring to the team and vision?

SP: Hiring Amanda demonstrates our commitment to compliance and regulatory affairs. This is key as we position ourselves such that our B2B customers…and their attorneys…can rely on us to do our job in a compliant manner.

NB: BAKKT has been slowly but surely preparing for their launch, and it has been met with a lot of excitement. In your mind, what is the significance of the BAKKT launch?

SP: It’s the first major, institutional-quality custodian launching in the digital market. Naturally I consider Prime Trust to be institutional-quality, but let’s be realistic as in terms of media, market and customer perception there is little question but that the affiliate of the NYSE carries a lot of credibility. They will get their share of the business, but I view them more as helping the market in general than competing with us in particular – we each do things that the other doesn’t.

NB: NovaBlock is very excited about the idea of tokenizing traditional assets: real estate, commodities, stocks, bonds, etc. What is required for asset tokenization to become the norm for issuance and secondary trading? What is currently keeping this segment of the industry back from wider adoption?

SP: The single biggest things that are needed:

a. an ATS that embraces trading private securities and develops the buy-side. From my perspective, real-estate is a natural first-product for this; and,

b. custodians who hold these private securities in customer accounts and who provide API’s that the ATS can write into for effecting transactions, confirming delivery, and settling trades (not to mention assuring compliance with tax obligations of investors). Prime Trust is currently the only one that I know of which provides this, and there needs to be others (which will happen). The custodians then need to work together to ensure counterparty settlements.